hy Insurance Is Quietly Deciding Which Homes Florida Buyers Can Afford

There’s a cost hiding inside every Florida real estate transaction right now.

It’s not the mortgage. It’s not the taxes. It’s not even the price of the home.

It’s insurance — and it’s quietly disqualifying properties, killing deals, and reshaping which homes buyers can actually afford to own.

The Number That’s Rewriting Florida Real Estate

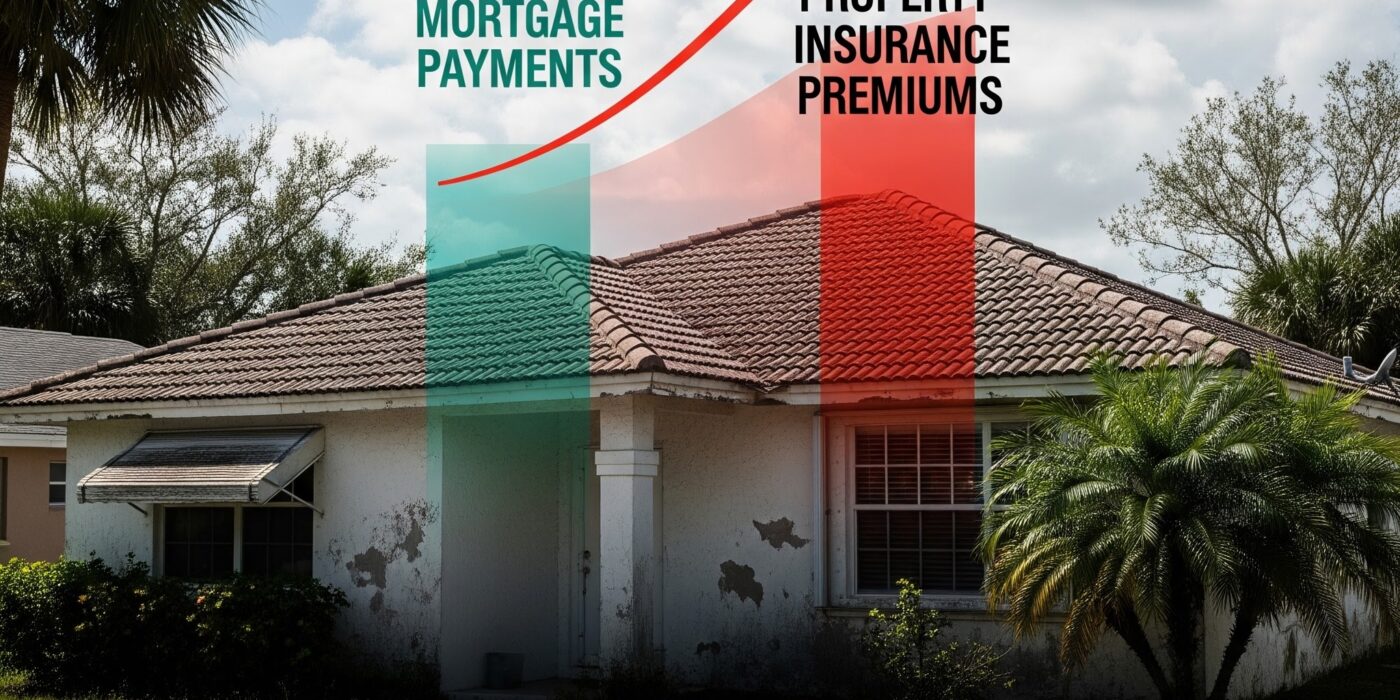

Here’s a sentence that would have been unthinkable a decade ago: in parts of Florida, annual property insurance premiums are now exceeding mortgage payments.

That’s not hyperbole. That’s the lived reality for homeowners in high-risk coastal zones where carriers have either exited the market entirely or repriced coverage to reflect what they now understand about Florida’s climate trajectory.

Nearly half of all real estate agents in Florida report insurance issues actively derailing transactions. Not slowing them down. Derailing them. Deals that survive the inspection, the appraisal, and the financing contingency are collapsing at the closing table because the insurance quote came back at a number the buyer’s monthly budget simply can’t absorb.

The market has quietly reorganized itself around this reality.

And most buyers — and too many builders — haven’t caught up yet.

How Insurance Became the Invisible Gatekeeper

For most of Florida’s modern real estate history, insurance was a line item. Buyers budgeted for it the way they budgeted for HOA fees — an inconvenience, not a deal-breaker.

That changed with a combination of forces that arrived in rapid succession.

First, a wave of major insurers exited the Florida market, leaving Citizens Insurance and a shrinking pool of private carriers to absorb demand they weren’t structured to handle. Then the Surfside collapse in 2021 triggered sweeping condo safety mandates that doubled and tripled association fees overnight — adding an entirely new layer of carrying cost on top of already elevated premiums.

Then came the hurricanes. Ian. Helene. A succession of storms that forced every underwriter still operating in Florida to recalibrate their risk models from scratch.

The result: insurance is no longer priced on historical averages. It’s priced on forward-looking risk — and in Florida, that number keeps moving in one direction.

Escrow payments increased by 14% in 2024 alone, driven almost entirely by insurance cost acceleration. For financed buyers, that increase hit without warning, mid-ownership, in the form of a revised escrow statement.

For many, it was the financial breaking point.

The Pre-Showing Filter Nobody Talks About

Something is happening in Florida buyer behavior that the industry hasn’t fully accounted for yet.

Buyers are filtering properties by insurance viability before they ever schedule a showing.

Experienced agents are now reporting that serious buyers — particularly those who have owned Florida property before — are asking a specific set of questions before they request a tour:

- Does the home have impact windows and doors on every opening?

- What is the roof-to-wall connection rating?

- What flood zone is the property in, and what is the FEMA elevation certificate showing?

- Has the property filed insurance claims in the past five years?

If the answers don’t hold up, the property doesn’t make the shortlist. Not because the buyer dislikes it, but because they’ve done the math and the insurance cost makes the total ownership equation unworkable.

This is a structural change in how Florida real estate is being evaluated. The premium gap between an insurable property and an uninsurable one isn’t a negotiation point anymore. It’s a market segmentation line.

Properties on the wrong side of that line are sitting. Properties on the right side are moving.

What “Insurable by Design” Actually Means

The phrase sounds like marketing. It’s actually engineering.

A home built with insurance performance in mind looks different from the foundation up:

Structural frame: Concrete and steel construction qualifies for significantly lower wind and fire premiums. Insurers assign direct cost reductions to buildings that won’t fail in a Category 4 event. This isn’t a soft discount — it’s a quantifiable reduction built into the underwriting model.

Openings: Every window, door, and garage entry rated for impact resistance removes a major pricing variable from the insurance equation. Properties without certified impact protection face premiums that can run double those of comparable protected homes.

Roof system: The connection between roof deck and wall structure is one of the most scrutinized elements in any Florida wind mitigation inspection. Modern engineered connections — designed to transfer load continuously to the foundation — translate directly into lower premiums on the wind mitigation report.

Flood elevation: Properties built above base flood elevation, particularly those in X flood zones rather than AE or VE zones, carry dramatically lower NFIP premiums. For buyers in coastal or near-coastal areas, elevation certificate data is now reviewed with the same scrutiny as a home inspection.

Build system: Factory-built and system-built components carry inherent quality consistency advantages. When an underwriter evaluates construction quality, precision-manufactured components carry less uncertainty than site-built assemblies subject to variable labor and weather conditions.

These aren’t luxury features. They are the baseline specifications of a home that can compete in today’s Florida market.

The Cost Math That Changes Everything

Here’s the calculation that sophisticated Florida buyers are running — and that developers need to understand:

A home built to conventional minimum code in a moderate-risk zone might carry an annual insurance premium of $8,000 to $12,000. The same square footage, same location, built with reinforced concrete, impact openings, and a certified wind mitigation profile, might carry a premium of $3,500 to $5,500.

That delta — $4,000 to $6,500 annually — represents $333 to $541 per month in real purchasing power.

At current mortgage rates, that monthly savings translates to approximately $60,000 to $100,000 in additional borrowing capacity for a financed buyer. Put differently, a buyer who can afford a $450,000 mortgage on a conventionally built home could qualify for and afford a $530,000 mortgage on a properly engineered one — because the total monthly cost of ownership is lower.

The more resilient, more expensive-to-build home is actually the more affordable one to own.

This is the argument that reframes the entire conversation about construction cost. The upfront investment in a properly engineered building system isn’t a premium. It’s a financial strategy.

What This Means for Developers and Builders

If you are building in Florida right now without insurance performance as a core design criterion, you are building into a narrowing market.

The buyers who remain active in this environment — cash buyers, international investors, storm-fatigued relocators making deliberate decisions — are among the most informed property buyers in the country. They have been educated by the market itself. They know what they’re looking for, and they know how to calculate what poor construction quality costs them over a ten-year hold.

They are not negotiating on features that protect their insurance position. They are walking away from properties that can’t provide one.

The developers who understand this are treating insurance performance the way the best builders have always treated structural integrity — not as a compliance exercise, but as a competitive advantage baked into every decision from site selection to material specification.

The ones who don’t are going to find that the Florida market has quietly moved on without them.

The Bottom Line

Insurance didn’t used to decide which homes Florida buyers could afford.

It does now.

The question for every developer, builder, and investor operating in this market is simple: are you building homes that work inside today’s insurance reality — or homes that fight against it?

The answer will determine who captures the next cycle of Florida housing demand, and who spends the next three years watching inventory sit.

Are you seeing insurance reshape buyer behavior in your market? What construction decisions are your buyers asking about before anything else? Drop a comment or send a message — these conversations are shaping how the most forward-thinking builders in Florida are positioning right now.

#FloridaRealEstate #HousingAffordability #Constructonik #InsuranceCrisis #ResidentalDevelopment #FloridaDevelopment #ModernConstruction #ResilientHousing