What “Hurricane-Ready” Actually Means in Modern Florida Construction?

What “Hurricane-Ready” Actually Means in Modern Florida Construction

Every builder in Florida says their homes are built to withstand hurricanes.

It’s on the websites. It’s in the sales presentations. It’s the answer every prospect gets when they ask the question directly.

But when the storm makes landfall — when the wind load is real and the rain is horizontal and the pressure differential is testing every connection in the building — marketing language doesn’t hold anything together.

Engineering does.

The Problem With “Hurricane-Ready” as a Marketing Claim

Florida’s building code is among the most stringent in the country. That’s not in dispute. The post-Andrew reforms of the 1990s and the post-Charley, Frances, Ivan, and Jeanne cycle of 2004 produced a regulatory framework that genuinely raised the floor on residential construction quality.

But here’s what the floor actually means: it’s the minimum acceptable standard for a building permit, not a performance guarantee in a major storm event.

A home built to Florida minimum code will, in most cases, survive a Category 3 storm without catastrophic structural failure. That is a meaningful baseline. It is not, however, what a buyer asking about hurricane resistance is actually asking about.

What they’re asking — particularly buyers who have watched Southwest Florida absorb Hurricane Ian, who have seen the images from Lee County, who have friends and colleagues who lost homes they were told were hurricane-ready — is something more specific:

Will this building perform? Not just survive. Perform.

The gap between surviving and performing is where the real conversation about modern Florida construction begins.

What Minimum Code Actually Covers — And What It Doesn’t

To understand what hurricane-ready should mean, it’s worth being precise about what current Florida building code actually requires and where its limitations lie.

Florida’s High Velocity Hurricane Zone requirements — applied to Miami-Dade and Broward counties — represent the most demanding residential code in the United States. The Florida Building Code Wind Speed maps designate design wind speeds by geography, and construction in most coastal and near-coastal areas must meet 130 to 160 mph design standards.

What that means in practice:

- Structural framing must be engineered to resist calculated wind loads

- Roof assemblies must use specific fastening patterns and sheathing specifications

- Openings must be protected or use impact-resistant glazing in designated zones

- Roof-to-wall connections must meet minimum uplift resistance requirements

What that doesn’t guarantee:

- That the home will sustain no damage in a major storm

- That the roof system won’t experience partial failure under sustained Category 4 or 5 conditions

- That water intrusion won’t occur through code-compliant but imperfect envelope assemblies

- That the accumulated effect of wind, rain, and pressure over a multi-hour storm event won’t compromise systems that passed inspection individually

Minimum code is a threshold. It is not a performance standard. And in a state where the question is no longer whether a major hurricane will arrive but when, the distinction matters enormously.

The Five Elements of Genuine Structural Resilience

A building that is genuinely engineered for Florida’s hurricane environment — not just code-compliant, but performance-designed — looks different across five specific dimensions.

- The Structural System

The most foundational decision in hurricane-resilient construction is the primary structural material. Concrete and steel construction outperforms wood-frame in hurricane conditions not because of code requirements but because of physics.

Concrete doesn’t fail progressively the way wood-frame does. It doesn’t absorb moisture that compromises structural integrity over time. It doesn’t create the combustion risk that makes post-storm fires such a significant secondary hazard. And in a wind event, mass matters — the inertia of a concrete structural system resists the racking forces that cause wood-frame buildings to deform under sustained load.

Reinforced concrete and structural steel aren’t premium upgrades in Florida’s climate. They are the rational material choice for a building system designed to perform in the environment it actually occupies.

- The Continuous Load Path

This is where most conversations about hurricane resistance stop being general and start being specific — and it’s where real engineering separates from marketing language.

A continuous load path means exactly what it says: the wind forces acting on a building are transferred continuously and without interruption from the roof through the walls through the floor system to the foundation. Every connection in that chain is engineered to handle the load. No weak link.

In a hurricane, the forces acting on a building aren’t static. They are dynamic, directional, and fluctuating. Uplift forces try to separate the roof from the wall. Lateral forces try to rack the wall off the foundation. Internal pressure — driven by any breach in the envelope — amplifies both.

A building with a genuine continuous load path resists all of these forces simultaneously. A building where one connection in the chain is undersized, under-fastened, or improperly detailed will fail at that connection — often catastrophically and suddenly.

The difference between a home that loses its roof in Ian and one that doesn’t frequently comes down to a single connection detail that was or wasn’t engineered correctly.

- The Envelope System

The building envelope — every opening, every joint, every transition between materials — is the hurricane’s primary point of attack.

Impact-resistant windows and doors rated to Florida Product Approval standards aren’t optional features for buyers in Florida’s coastal and near-coastal markets. They are the baseline specification for a building that will maintain envelope integrity in a major storm.

But impact glazing alone isn’t sufficient. The installation — the frame anchoring, the sealant system, the integration with the wall assembly — determines whether the rated performance is actually delivered. A properly rated window installed incorrectly will fail before its rating is reached.

Roof-to-deck connections, ridge cap systems, soffit and fascia detailing — these envelope elements are consistently where water intrusion begins during storm events. A genuinely hurricane-resilient building treats every envelope transition as a potential failure point and engineers accordingly.

- The Foundation System

In Florida’s flood-risk environment, foundation design carries two distinct performance requirements: structural resistance to wind-induced uplift and lateral forces, and elevation above base flood levels sufficient to prevent or minimize flood intrusion.

Elevated foundations — pilings or stem walls that position the living space above base flood elevation — don’t just reduce flood damage. They reduce flood insurance premiums, often dramatically. For buyers in AE or VE flood zones, the foundation decision has direct and quantifiable financial implications for the life of ownership.

A building designed for Florida’s actual risk environment treats foundation engineering as a performance specification, not a compliance exercise.

- The Mechanical and Systems Integration

The structure can perform perfectly and a building can still be rendered uninhabitable if its mechanical systems aren’t integrated with the same resilience intent.

HVAC systems located in unconditioned attic spaces are vulnerable to roof damage. Electrical panels positioned in flood-prone locations create recovery delays that extend displacement by weeks. Backup power systems — whether generator connections or solar-plus-battery integration — determine whether a home is livable in the days immediately following a storm.

A genuinely hurricane-ready home thinks about the recovery experience, not just the storm survival moment. The goal isn’t just to be standing when the storm passes. It’s to be functional.

Why This Is Now a Baseline Conversation, Not a Premium One

Here’s the market reality that has shifted the entire framing of this conversation.

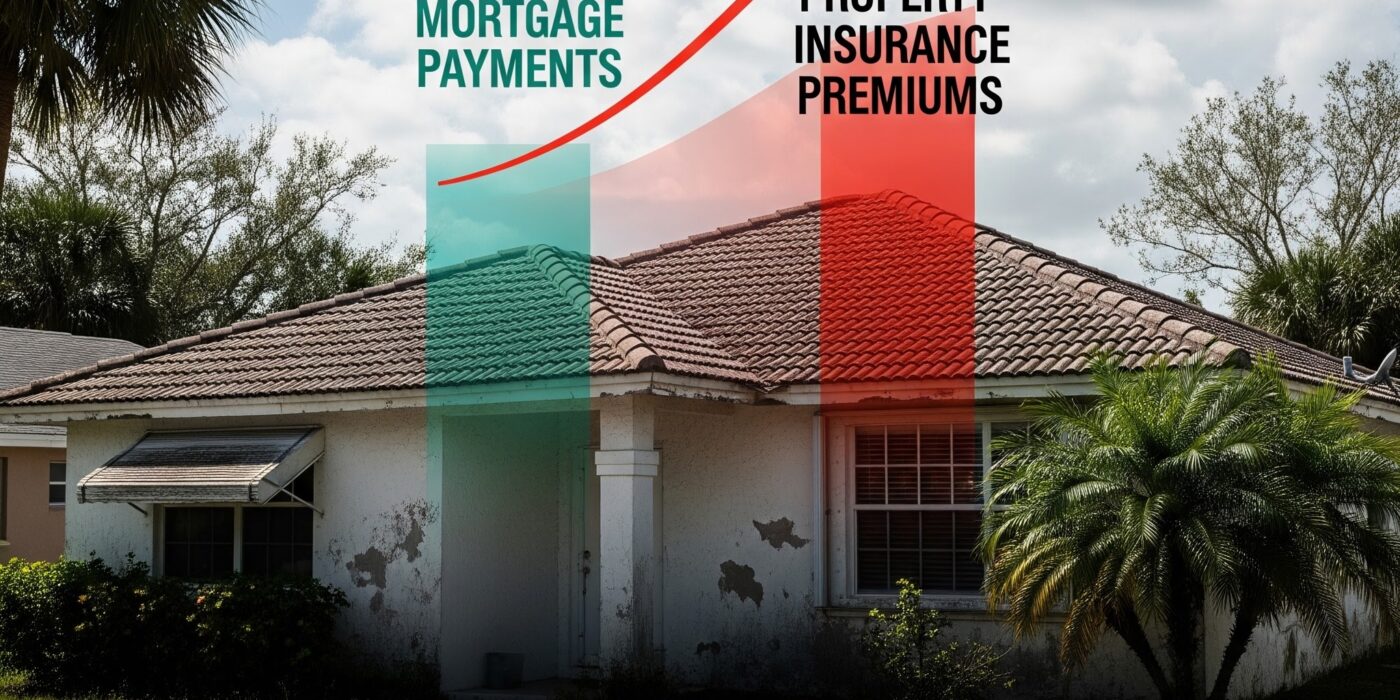

Florida buyers in 2026 are not asking whether a home is hurricane-resistant as a way to evaluate an upgrade. They’re asking because they understand that a home without genuine resilience engineering is a financial liability — not just a safety concern.

The insurance market has formalized this understanding. Wind mitigation inspections now directly translate construction quality into premium dollars. A home with a documented continuous load path, certified impact openings, and a rated roof-to-wall connection system earns quantifiable premium reductions. A home without those features pays the penalty — indefinitely.

The buyer who has watched neighbors spend eighteen months in temporary housing while their “code-compliant” home was rebuilt is not interested in minimum standards. They are interested in performance.

And the developer or builder who can speak specifically — not in marketing language but in engineering language — about how their building system addresses each of the five dimensions above is speaking the language that this buyer understands and responds to.

The Standard Has Moved

Florida’s hurricane history has been an ongoing education for everyone in the built environment.

Each major storm event has revealed specific failure modes. Each revelation has informed better engineering. The developers and builders who are paying attention to that education — who are treating each storm as a full-scale performance test of construction methodology — are building differently than they were a decade ago.

The ones who aren’t are still using “hurricane-ready” as a marketing claim.

The difference will be apparent the next time a major storm makes landfall in Florida.

It always is.

What specific construction standards are you requiring on your Florida projects right now? Are your buyers asking more sophisticated questions about structural performance than they were two years ago? Drop a comment or send a message — the engineering conversation is becoming the most important one in Florida real estate development.

#FloridaRealEstate #HurricaneReady #Constructonik #StructuralResilience #FloridaDevelopment #ModernConstruction #HousingInnovation #ResilientBuilding