The Real Cost of Owning a Home in Florida Isn’t the Price Tag

The Real Cost of Owning a Home in Florida Isn’t the Price Tag

Most buyers negotiate hard on purchase price.

They spend weeks comparing listings, making offers, pushing back on counteroffers — trying to save $10,000, maybe $20,000 on the contract number.

Then they spend the next ten years paying for a decision they made in an afternoon.

The Number on the Listing Isn’t the Number That Matters

Florida real estate has always attracted buyers who know how to read a market. Investors who understand cap rates. Developers who model IRR before they make an offer. Professionals who have done this before.

And yet, even sophisticated buyers regularly underestimate the true cost of owning a home in Florida — because the purchase price is the most visible number in the transaction, and visibility creates a false sense of importance.

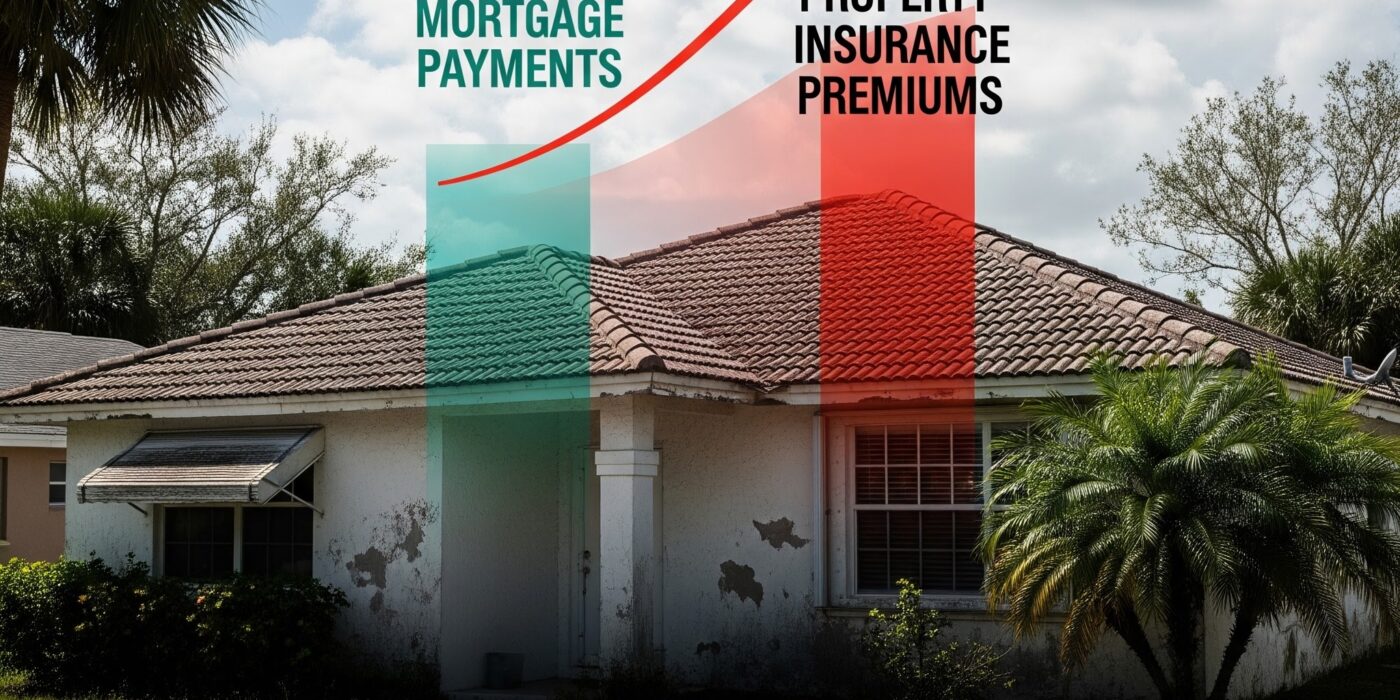

The number that actually determines whether a Florida home is affordable isn’t the price tag.

It’s the total monthly cost of ownership over a 10-year hold.

When you calculate that number honestly — insurance, energy, maintenance, HOA trajectory, and the probability of unplanned repair — the hierarchy of what makes a good Florida real estate decision changes completely.

What Total Cost of Ownership Actually Includes

Let’s be precise about what we’re measuring, because vague financial thinking is how buyers end up underwater on properties that looked affordable at signing.

Property insurance: In Florida’s current market, this is no longer a stable, predictable line item. Homeowners in high-risk zones are carrying premiums of $8,000 to $15,000 annually — and those numbers have been moving upward consistently. Escrow payments increased 14% in 2024 alone. A buyer who budgeted $6,000 per year for insurance three years ago may be paying $11,000 today, with no structural reason to expect it to stabilize.

Energy costs: Florida’s utility environment is not forgiving. Air conditioning runs nine to ten months of the year in South and Central Florida. A home with poor insulation, single-pane windows, or an aging HVAC system can carry monthly utility costs of $400 to $600 or more. Over ten years, the gap between an energy-efficient home and an inefficient one can represent $30,000 to $50,000 in cumulative cost.

Maintenance and repair: Conventional site-built construction in Florida carries ongoing maintenance demands that buyers rarely budget for honestly. Roof replacement, exterior paint, wood rot remediation, HVAC servicing, and plumbing degradation are not exceptional events. They are the predictable output of building systems that weren’t designed for Florida’s humidity, heat, and storm exposure. Industry estimates place annual maintenance costs for a conventionally built Florida home at 1% to 2% of home value annually — meaning a $450,000 home should be budgeted at $4,500 to $9,000 per year in maintenance.

HOA and assessment trajectory: For condo owners specifically, this line item has become a financial crisis. Post-Surfside safety mandates have doubled and tripled association fees almost overnight. Special assessments reaching tens of thousands of dollars per unit are forcing owners on fixed incomes to choose between their savings and their homes. The Florida condo market is now described by analysts as the worst performing since the 2008 financial crisis — driven almost entirely by carrying cost escalation, not purchase price.

Storm damage exposure: This is the cost that traditional pro formas almost never include — but that Florida homeowners pay with disturbing regularity. A conventionally built home in Southwest Florida that sustained damage in Hurricane Ian and required partial rebuild is carrying a cost that dwarfs any negotiation savings achieved at contract. That cost isn’t theoretical for thousands of Florida homeowners right now. It’s real, and it arrived without warning.

When you add these figures together, the picture changes substantially.

The Math That Reframes the Conversation

Here’s a direct comparison that illustrates why purchase price is the wrong lens for evaluating Florida real estate.

Home A: $420,000 purchase price. Conventionally built, 2005 construction. Single-pane windows, standard wood-frame construction, no impact protection. Insurance: $11,000 per year. Energy: $550 per month. Maintenance budget: $7,500 per year. No wind mitigation certification.

Home B: $465,000 purchase price. System-built, engineered construction. Concrete structural system, impact openings throughout, wind mitigation certified, high-performance insulation. Insurance: $4,500 per year. Energy: $220 per month. Maintenance budget: $2,800 per year.

Home A costs $45,000 less at purchase.

Over ten years, Home A costs approximately $112,000 more to own.

The cheaper home is the more expensive asset. The math isn’t subtle — it’s decisive. And yet the Florida market continues to price and present homes primarily on the listing number, leaving buyers to discover the real cost of ownership after the contract is signed.

Why This Dynamic Is Particularly Acute Right Now

The total cost of ownership gap between well-built and poorly-built Florida homes has always existed. What’s changed is the magnitude of that gap — and how quickly it’s widening.

Three converging factors are accelerating the divergence:

Insurance repricing is ongoing. Carriers have not finished adjusting their Florida risk models. The stabilization of Citizens Insurance premium growth in 2025 was welcome news, but it doesn’t reverse the multi-year repricing cycle that is still working through the market. Homes without structural resilience features will continue to face premium pressure.

Energy costs are not declining. Florida utility rates have increased consistently, and the performance gap between an energy-efficient building envelope and a conventional one grows more financially significant every year. A home built with structurally insulated panels or insulated concrete forms doesn’t just perform better today — its advantage compounds annually as energy costs rise.

The maintenance gap is becoming visible. Florida’s post-pandemic construction boom produced a significant volume of housing built under cost and labor pressures that compromised quality in ways that are only now becoming apparent. Buyers and investors who purchased conventionally built homes in 2021 and 2022 are beginning to encounter the maintenance consequences of that era. The repair bills are arriving.

What Smart Buyers and Developers Are Calculating Instead

The most sophisticated buyers currently active in the Florida market have moved past purchase price as their primary evaluation metric.

What they’re calculating:

- Insured cost of ownership — the total monthly outlay including insurance, not just mortgage and taxes

- Energy performance rating — utility cost projections based on building envelope and mechanical specifications, not assumptions

- Structural longevity — the expected maintenance and replacement cycle for every major building system

- Insurance qualification profile — wind mitigation rating, flood zone status, impact protection certification, and the direct premium implications of each

- Residual value trajectory — how the home’s construction quality positions it in a market where buyers are increasingly filtering by insurability and resilience

This is not overcomplicated analysis. It’s the analysis that every commercial real estate investor applies to every acquisition decision. It’s simply being applied to residential real estate in Florida because the market has made it necessary.

The buyers running this math are making better decisions. They’re also negotiating from a position of genuine understanding — which means they’re identifying value where other buyers see only price, and risk where other buyers see only opportunity.

The Implication for Developers and Builders

If you are developing or building in Florida without modeling total cost of ownership as a core marketing and product development input, you are missing the most compelling value argument available to you right now.

The conversation has shifted. Buyers are no longer simply comparing purchase prices. They are — increasingly — comparing ownership costs. And a home that costs more to buy but dramatically less to own is not a hard sell to a financially literate buyer.

It’s the easiest sell in the market.

The developers who build this case into their sales process — who can present a credible, specific, line-item comparison between their product’s ownership cost and a conventional alternative — are not just differentiating on features. They are differentiating on financial logic.

In a market full of listings competing on price, that is a category-defining advantage.

The Question Worth Asking Before Every Transaction

Before any Florida real estate decision — purchase, development, or investment — one question should precede all others:

What does this actually cost to own?

Not to buy. To own.

The answer to that question is where the real decision lives. And in today’s Florida market, it’s the question that separates buyers who build long-term wealth from those who simply transfer it to someone else.

How are you modeling total cost of ownership in your Florida real estate decisions? Are your buyers asking these questions yet — or are they still negotiating on price? Drop a comment or send a message. The developers having this conversation with their buyers right now are building a significant competitive advantage.

#FloridaRealEstate #TotalCostOfOwnership #Constructonik #RealEstateInvesting #FloridaDevelopment #HousingAffordability #ModernConstruction #SmartBuilding